Download Reports

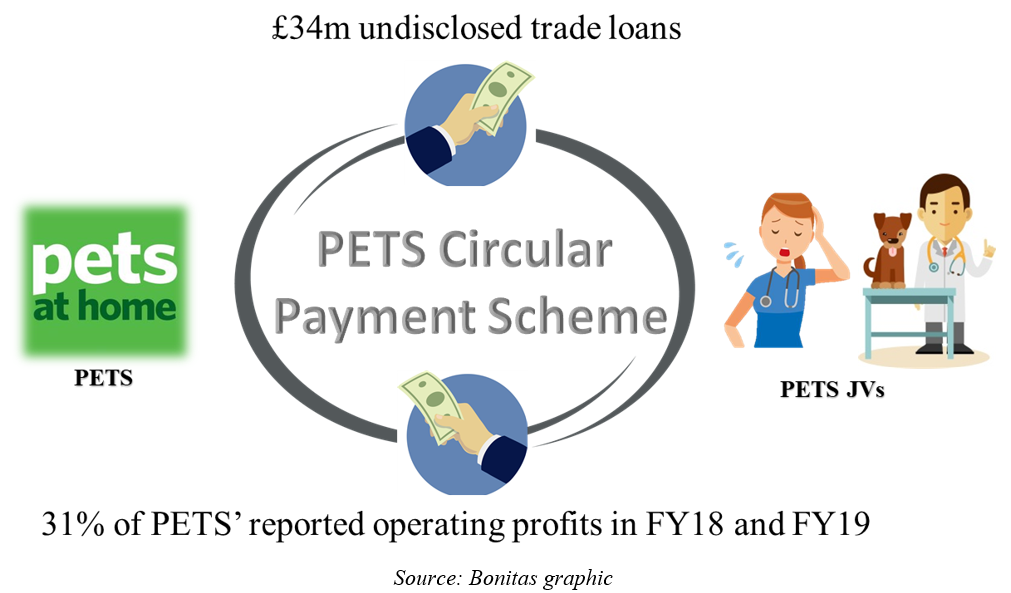

May 12, 2020 - Short Pets At Home (London: PETS)UK Companies House filings revealed that Pets at Home Group Plc (LSE: PETS) (“PETS”) lied about GBP 34 million of undisclosed trading loans hidden from its balance sheet used to support circular payments from PETS Vet Group Joint Ventures (“PETS JVs”) which we believe artificially inflated PETS reported profits.

Including undisclosed trading balances, PETS’ actual funding, trading and operating (“FTO”) loan balances owed by PETS JVs were GBP 74 million and GBP 64 million as of FYE’18 and FYE’19, 87% and 51% greater than what PETS reported in its FY’19 Annual Report. Without these loans, PETS JVs would not have been able to pay PETS service fees and rents.

The circular payment scheme had a significant impact on PETS’ purported profitability. PETS recognized 50%+ operating margins on PETS JV service fees versus 8% for its retail segment. While accounting for only 6% of PETS revenues, PETS JV service fees accounted for 31% of PETS’ operating profits.

We reviewed over 1,800 annual reports for 432 individual PETS JVs between FY’15 and FY’19 available for free online via UK Companies House filings. Most PETS JVs were loss-making and drowning in liabilities. In FY’18, while PETS generated GBP 27 million operating profits from PETS JV service fees, PETS JVs generated aggregate losses of GBP 14 million. PETS JVs revealed aggregate liabilities of GBP 170 million as of FYE’19.

Recently PETS actively restructured some PETS JVs via step-up acquisitions and in each instance PETS assumed all PETS JV liabilities. PETS’ restructuring efforts have already cost GBP 40+ million in write-offs and expenses from 55 PETS JV step-up acquisitions as of FYE’19. As PETS JVs sink deeper into debt, we anticipate that PETS will be forced to bail out and write off additional PETS JVs.

Below are additional highlights from our review of operating PETS JV annual reports:

- 253 (61%) generated aggregate losses of GBP 27 million in FY’18.

- 108 (26%) had adminstrative expenses that exceeded revenues in FY’18.

- 283 (69%) were balance sheet insolvent with aggregate net liabilities of GBP 100 million as of FYE’19.

- 60 (15%) had net liabilities that exceeded GBP 500,000 as of FYE’19 (not including 19 additional PETS JVs that were bought back and written off by PETS in FY’19).

PETS charged PETS JVs service fees and rents only afforded with concurrent financial support. If PETS cannot continue to provide such a significant level of financial support to PETS JVs, the scheme collapses.

Source: Bonitas graphic

PETS’ FYE’19 balance sheet held GBP 395 million goodwill largely attributable to the future cash flow generating ability of PETS JVs and reported a contingent liability of GBP 11 million, only 17% of what PETS JVs owed third party banks.

To us, the evidence is clear that PETS lied to investors about the level of financial support given to PETS JVs which artificially inflated PETS’ reported profitability and understated its liabilities. We believe a restatement of PETS’ financial performance would include adjustments to goodwill, increased recognized exposure to PETS JV bank debt and further write-offs of direct loans to PETS JVs.

As investors consider PETS’ hidden liabilities, its low earnings quality from circular payments and inflated carrying balances for certain assets, we think PETS’ stock price could break previous lows with a downside of 75%+.